In economics, the terms “Supply” and “Demand” are of fundamental importance to the discipline because they are the factors that drive all other related activities of the economy. Argumentatively, although the field is broad and these two are like the pillars that hold together everything else in place, the exchange of goods and services from the seller side and the buyer’s side. Simply put, the demand covers the customer side while the supply side covers the seller’s side, who provide the goods or service. So, this, paper will discuss in detail the two terms and extensively cover what they mean in the context of economic transactions and how they relate. Also, the paper will seek to explore the shifts in demand and supply; because they are not static but are subject to changes of either going up or going down- for both depending on various factors that will form part of the subsequent discussions of this paper.

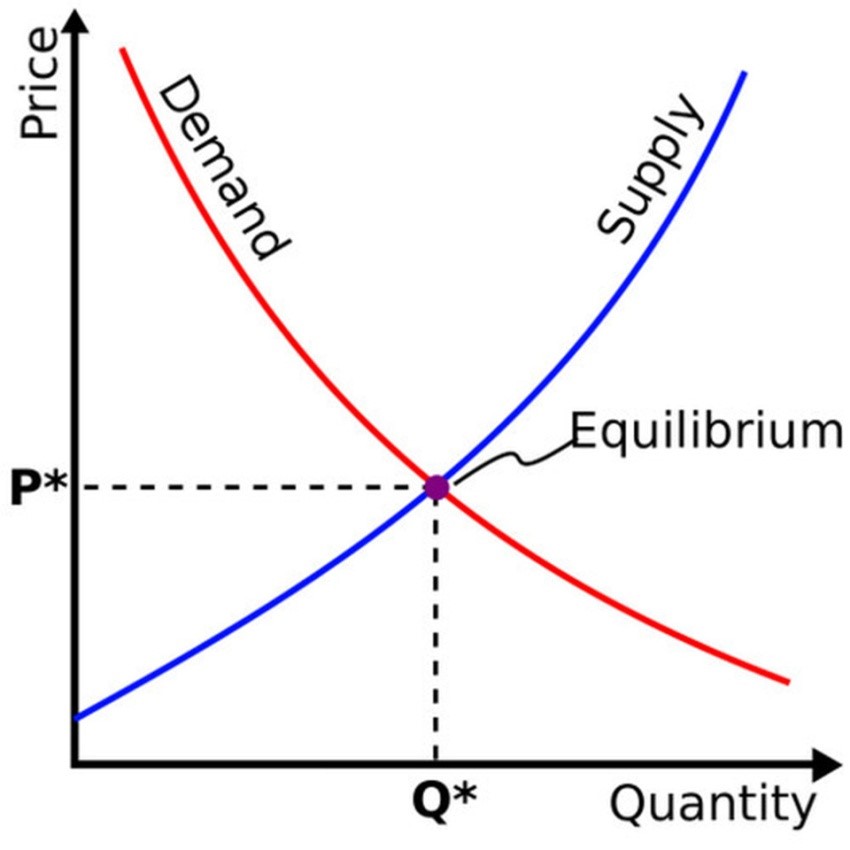

At this point, it is important to note while they are closely related, it is not automatic that an increase will one will cause the same reaction for the other. Each independently responds differently to certain factors. However, in a state of equilibrium, the shifts are similar where if demand, increases the seller responds also by increasing their goods or services(Bas, et al. 4). For each, the discussions will revolve around meaning, application in the real-life, and the relationship with the causal agents that leads to particular changes. The figure below shows the relationship between demand and supply that will guide the subsequent discussions.

Figure 1 Relationship between Demand and Supply

Demand in the field of economics refers to the total amount of goods or services that consumers are able and willing to pay for it when it is at that price. In practice, demand is usually different at each price level which is the main factor that influences the patterns of consumers’ behavior. The price is used as the reference point of explanation because it usually reflects the value of a product and its utility preference to the buyer. In particular, just how much is a customer willing to pay and what amount of the product or service do they want for it at that price is what demand is all about(Bas, et al. 11). In some of the cases, a customer attending a fair on a hot day may be willing to pay more for a glass of lemonade than if they had attended the fair when the weather was cold. So, demand is the total amount of product that a consumer will be expecting in return for money of a certain value.

At different prices, the quantity will change because of the different factors mentioned in the subsequent parts of the paper. From this example, it is clear that the demands thus also exist at different levels; the first is the market demand for the product itself in the economy and the second is the aggregate collective demand of all the products that exist in the market for that economy. In the first level, the focus is the product itself in the context of the consumer, and for the second, it is all the products that are present in that specific jurisdiction. A good example is a demand for a GTI muscle automobile in the US may be 15 % while the demand for all cars in the US is 56%. Therefore, in the first example, the particular product is assessed individually within the context of the market while in the second level it is all products that the same, i.e. cars, that are calculated.

Supply, on the other hand as aforementioned represents the other side of the economic transaction divide, the suppliers. The suppliers’ framework is overly broad and is used to refer to all such factors that are elements of production including labor, money, and companies that collectively produce the goods to the buyer. Supply: therefore, this definition refers to the total amount of goods and services that the supplier is willing to produce and offer to the market at a certain price (Moheb-Alizadeh and Handfield 5). Using the earlier example, now the seller of the lemonade at the fair is willing to make a certain amount of the drink for the market at a particular price. So, for example, if the fair is hosted on a sunny day, the price is higher and thus he or she may be willing to produce more lemonade for the fairgoers. However, on a cold day when the price of the lemonade is lower, he may only be willing to produce a lower amount of lower to reduce. The price is used as the central incentive in an economy that is why in both cases it is the principal elements that are used to define both supply and demand. As stated earlier, the movements are not static but rather shift according to different factors.

The shifts in the demand and supply of the goods and services for a particular product is dependent primarily on the prices of the inputs that are used in the production of the goods and services such as labor, raw materials, tariffs attached to the product and technical resources involved in the production. Similarly, for the demand for a good or service shifts according to the prices set for the product or service (Mankiw 54). When the prices are higher and other factors remain constant regarding the product, the demand reduces and when the prices reduce, the demand increases. From this point of view, it is accurate to hypothesize that demand and supply shifts according to how the prices move when all other factors remain constant.

Works Cited

Bas, M., et al. “From micro to macro: Demand, supply, and heterogeneity in the trade elasticity.” Journal of International Economics, vol. 108, 2017, pp. 1-19, doi:10.1016/j.jinteco.2017.05.001.

Mankiw, N. G. Essentials of economics. Cengage Learning, 2020.

Moheb-Alizadeh, H., and R. Handfield. “Developing talent from a supply–demand perspective: An optimization model for managers.” Logistics, vol. 1, no. 1, 2017, p. 5, doi:10.3390/logistics1010005.

write

write